Transaction Center

Time to bring it home. Find zipForm®, transaction tools, and all the closing resources you'll need. Except for the champagne — that's on you.

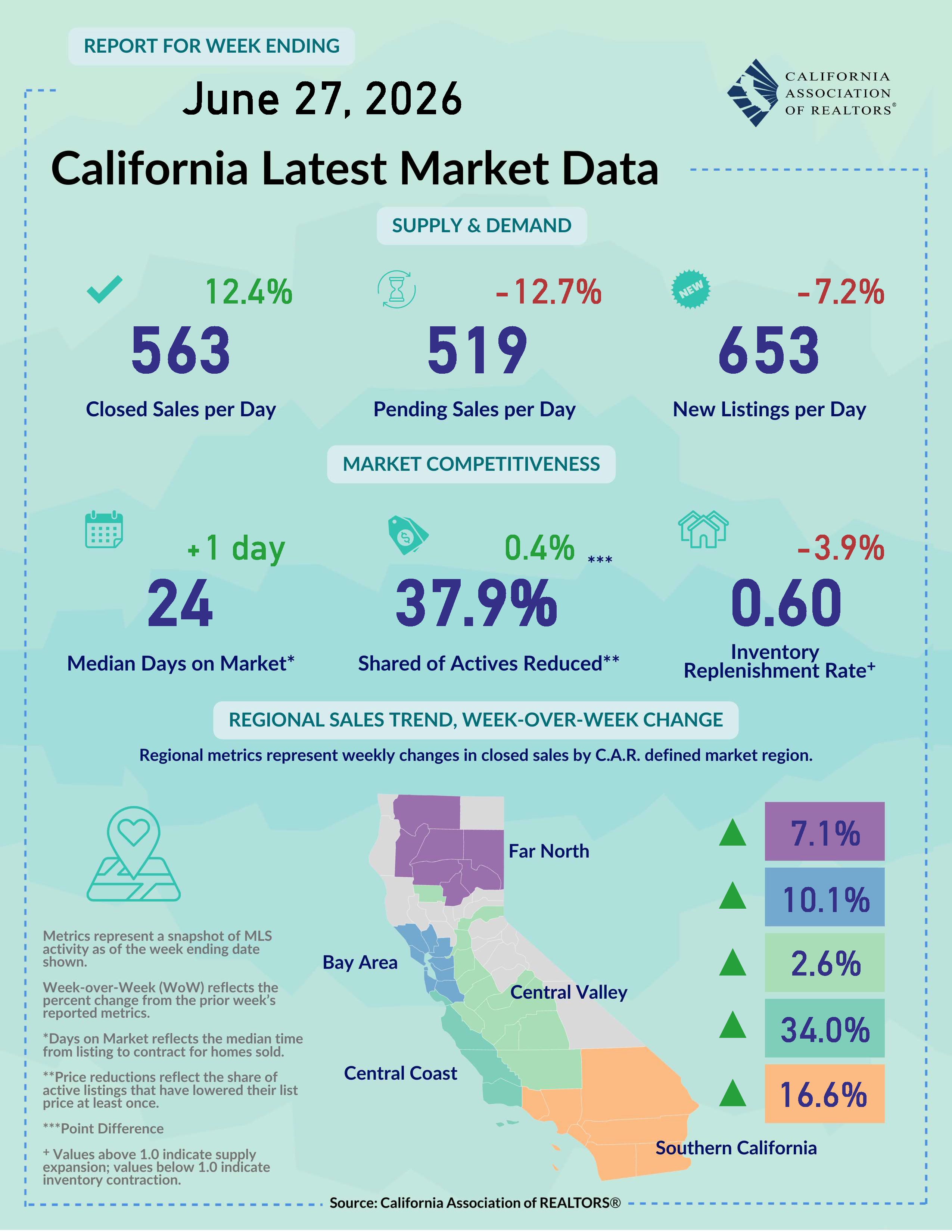

View the latest sales and price numbers. Find out where sales will be in upcoming months.

Get a roundup of weekly economic and market news that matters to real estate and your business.

Gain insights through interactive dashboards and downloadable infographic reports.

All Shareable Reports All Interactive DashboardsCatch up with the latest outreaches and webinars by the Research and Economics team.

C.A.R. conducts survey research with members and consumers on a regular basis to get a better understanding of the housing market and the real estate industry.

California Model MLS Rules, Issues Briefing Papers, and other articles and materials related to MLS policy.

Looking for information on how to file an interboard arbitration complaint? You've come to the right place! Find the rules, timeline and filing documents here.

Summaries and photos of California REALTORS® who violated the Code of Ethics and were disciplined with a fine, letter of reprimand, suspension, or expulsion.

The most recent edition of the Code of Ethics and Standards of Practice of the National Association of REALTORS® along with other important links to NAR information.

The California Professional Standards Reference Manual, Local Association Forms, NAR materials and other materials related to Code of Ethics enforcement and arbitration.

C.A.R. advocates for REALTOR® issues in Washington D.C., Sacramento and in city and county governments throughout California.

CREPAC, LCRC, IMPAC, ALF and the RAF comprise C.A.R.'s political fundraising arm.

The RAA: Protecting REALTORS® and Homeownership REALTOR® Action FundC.A.R. Senior Vice President Sanjay Wagle sits down with former Senate Majority Leader Emeritus Robert Hertzberg to discuss the proposed Middle-Class Homeownership and Family Home Construction Act.

Learn how you can make a difference, by getting involved yourself or by passing along valuable information to your clients.

|

June 29, 2026 - Recent housing and economic indicators offer some encouraging signs, even as uncertainty and affordability barriers remain issues in the next six months. Consumers are showing renewed interest in homeownership, AI is helping buyers navigate the process more efficiently, and softer energy prices are lifting sentiment from recent lows. Meanwhile, real estate professionals continue to play an important role by helping consumers make sense of market conditions and evaluate options through the homebuying process. Despite the market outlook turning slightly more positive in the past week, elevated mortgage rates and cost-of-living pressures will continue to weigh on the market. As such, improvement in the second half of 2026 should be gradual and dependent on further progress on inflation and buyer confidence. Americans feel more positive about homeownership despite affordability challenges: Homeownership sentiment improves from last year as more consumers say it is better to buy than to rent, according to the 2026 Bank of America Homebuyer Insights Report. The study shows that more than half (53%) of Americans favor buying a home over renting or moving in with family (47%). The share who says buying is better improves from last year’s 48% and it is the first time since 2023 that it exceeds the share of renting/moving in with family. Homeownership sentiment improves from last year across all measures, with 94% saying homeownership provides stability, 90% saying home is a valuable investment, and 32% saying that they are more confident in their ability to buy a home this year. Despite the rise in optimism, an increasing number of consumers say that expensive home prices (58%) and higher interest rates (47%) are the top factors that delay their home purchases. AI reshaping the homebuying process but not replacing real estate agents: The 2026 Bank of America Homebuyer Insights Report also indicates that AI is playing a growing role in the homebuying process, as 20% of prospective buyers and current homeowners used AI for homebuying research in the past 12 months. Some of the common usages of AI include estimating affordability, mortgage payments, or closing costs (57%), education and research about the homebuying process (55%), and research on neighborhoods/market trends/property values (52%). Many of them, however, still prefer to use a human expert for steps such as touring homes (55%) and legal/contractual advice (54%). So, while AI can streamline and enhance the homebuying journey, it is the trust and human connection that ultimately turn a transaction into a closed deal. Young LGBTQ+ adults expected to trail their heterosexual peers in entering homeownership: Gen Zers who are part of the LGBTQ+ community will likely fall behind in access to homeownership, as an LGBTQ+ Real Estate Alliance’s report indicates. According to the study, a majority of respondents expect heterosexual Gen Z individuals to advance more quickly in getting a work promotion, building wealth, and entering homeownership than an LGBTQ+ person. Nearly four of five of respondents believe heterosexual individuals are more likely than their LGBTQ+ peers to receive family financial support such as inheritance or down payment assistance. The lack of familial support could be a reason for the delay in homeownership for Gen Zer in the LGBTQ+ community. In fact, 69.6% of all respondents expect heterosexual individuals to buy their first home before the age of 35, as compared to 43.2% for LGBTQ+ young people. The discrepancy in optimism on entering homeownership between the two groups also affects how they define their American Dream. Homeownership is ranked number one of the defining assets for heterosexual young adults in attaining the American Dream but is not even ranked in the top five for LGBTQ+ individuals. With 23% of adults under 30-year-old identifying themselves as part of the LGBTQ+ community, the disparities the study indicate could have serious implications on housing gap in the long run if there is no course correction soon. Consumer sentiment bounces back as energy prices moderate: Americans began to feel better as lower gas prices improved, according to the June’s University of Michigan’s consumer sentiment index. Last month’s reading climbed 10% to 49.5 from May’s record low of 44.8 but remained the second lowest going back to at least late 1970’s. With concerns about the Middle East conflict easing, expectations on business conditions over the next five years soared 16% in June. Despite one-year inflation expectation inching down to 4.6% from 4.8% recorded in May, consumers remained concerned about the cost of living. For the third consecutive month, over half of them mentioned that higher prices are weighing down on their personal finances. With inflation likely to remain elevated in next few months but gradually coming down before the end of 2026, consumer sentiment should see moderate improvement in the second half of the year. New home sales decline for second straight month: Sales of newly constructed single-family homes in the U.S. declined 7.3% in May to a seasonally adjusted annualized rate of 580k, falling well below consensus expectations of 632k, as elevated mortgage rates and economic uncertainty kept many would-be buyers on the sideline. The drop in newly built home purchases in May was the second month in a row, and last month’s sales level reached the lowest since January when winter storms hit the housing market hard. On a year-over-year basis, new home sales were down 6.8% from May 2025. Three of four regions in the U.S. declined from a year ago, with the West falling the most by 17.0% from May 2025. With sales slowing, new-home inventory climbed to its highest level in years, pushing months of supply to 10.3 months from 9.3 months in April and 9.7 months in May 2025. Despite an increase in months of inventory, for-sale new housing units continued to decline by 1.4% from a year ago as developers have slowed down on building new homes due to concerns about their growing backlog of unsold homes. Home prices are holding up well for now, with the median price essentially unchanged from a year ago, but more downward pressure could be applied to prices if unsold inventory for new homes remain elevated in coming months. Note: This summary report gets updated every Monday by 6:00 pm PST. Feel free to email us at [email protected] if you have any questions and/or feedback.

|

|